If you’ve ever seen an ad talking about car financing, you may have noticed those companies saying anyone can apply and get approved, regardless of their credit score. We’ve done this as well. Some are skeptical of these kinds of offers so we wanted to dive in and explain further how this works.

The short answer is that it does work and it does make money. We know because we’ve already successfully connected thousands of customers (including those with sub-prime scores) to lenders so far in 2019. So let’s dive in.

Follow the money

Lenders make more money from people with lower credit scores. If you look at APR rates (governed by the “Truth In Lending Act of 1968, it also includes non-interest charges and fees so it gives you a more complete picture of the financing cost making it easier to compare loan proposals) per score, you will notice the change in rates:

| Category | New Car Rate | Change YoY | Used Car Rate | Change YoY |

|---|---|---|---|---|

| Total | 5.75% | +56 | 9.4% | +38 |

| Deep Subprime | 14.94% | +50 | 19.51% | -23 |

| Subprime | 12.14% | +79 | 16.72% | +24 |

| Nonprime | 7.55% | +63 | 10.63% | +57 |

| Prime | 4.45% | +48 | 5.94% | +52 |

| Super Prime | 3.47% | +42 | 4.19% | +51 |

The justification used for these higher rates is people with lower scores are higher risk, so for this higher risk, lenders want a better return on their money. But what is this higher risk?

Car Loan Delinquency

The lender’s main concern is getting their money back. They want to be as sure as possible that you’re going to keep up with payments and pay back the full amount + interest. When you start missing payments, that’s called delinquency but how bad is it?

We have a more detailed article about auto loan delinquencies in America, but the interesting part is that customers are less likely to miss a car payment than any other credit they may have and states can differ greatly (Washington DC has a delinquency rate of 7,23% while Minnesota has only 1,77%).

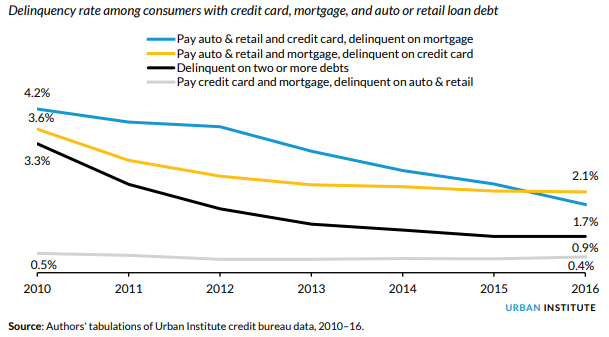

The Urban Institute put out an interesting paper about how people make loan repayment decisions when they start getting into trouble.

Consumers with all three loan types prioritized auto loans ahead of mortgages and credit cards, consistent with evidence from past work on payment preferences (Komos et al. 2012).

Delinquent Debt Decisions and Their Consequences over Time – Urban Institute

So if you combine high APR rates with a lower probability of missing payment vs. other credit types and you live in a state with a low average delinquency rate, it starts to make more sense for lenders to still consider customers with a poor credit scores because we prioritize repaying car loans over anything else (sorry student loans!).

Market Conditions

Last but not least, we can’t ignore the effect of the market and the monetary polices set by the government and the federal reserve. Since the great recession of 2008, markets have been flooded with cash and banks have been actively encouraged to lend money to revive the economy.

Once confidence started coming back, lenders have been on the lookout for more opportunities to take this money and find ways to lend it out. With these low interest rates and improved confidence, you get the perfect market conditions for almost anyone applying and getting the financing they need.

Final remarks

Even though it’s probably never been easier to get a car loan, regardless of your credit score, you could still end up paying relatively high APR rates if your score is too low. That’s why you should always consider the option of buying your car cash alongside possible financing options.

It pays to shop around and our site is an example of how you can fill out 1 profile and connect with hundreds of lenders, allowing you to compare and get best financing offer for you. It’s free and only takes a few minutes. As our economy keeps changing, so will the availability of loans so now is a good a time as any to start shopping around.